Module 2, lesson 1

Smart Budgeting for Incoming CMP Professionals

The CMP Industry is expensive: the pricey equipment, the rental fees, and all the other fees that you’ll encounter along the way. This lesson will explore the importance of smart budgeting and financial management for incoming CMP professionals.

objectives

- Learn the importance of financial management for young professionals

- Create a personal and professional budget

- Identify ways to allocate funds (savings, expenses, and investments)

The basics of budgeting

The CMP Industry is expensive: the pricey equipment, the rental fees, and all the other fees that you’ll encounter along the way. This lesson will explore the importance of smart budgeting and financial management for incoming CMP professionals.

A budget is an estimation of financial resources for a specified future period of time. Most, if not all CMP professionals believe it is a necessity to budget their expenses. It is an especially important practice for younger professionals with limited finances, because it can serve as a guide for important purchases and investments. Later in this lesson, we will review a step-by-step process of how to create a smart budget. For now, let’s take a look at the most important part of budgeting: saving money.

To have anything to budget in the first place, an essential skill is being able to manage your finances smartly. Even when your bank account seems to be overflowing, you must always view your money as a finite resource. Below are a few strategies to smartly save money:

- The 50-30-20 rule: Put 50% of your money toward needs, 30% toward wants, and 20% toward savings.

- The “pay yourself first” strategy: Each time you are tempted to make a purchase, put some money in your savings account too.

- Self-reflection: Like most decisions in our lives, it’s important to self-reflect before spending money. So before impulsively spending your money, ask yourself the following questions:

- If I do this, will I make more profit?

- If I don’t do this, will I make less profit?

- Should I do this because it fits with my values – even if I lose money as a result?

“It’s also about what you do in those down periods that would set you up for success for your busy periods as a creative. So kung ‘di ka nagtipid sa high periods mo, wala kang mararating pag nasa dry period ka na.” – Junessa Rendon

Preparing for the expenses

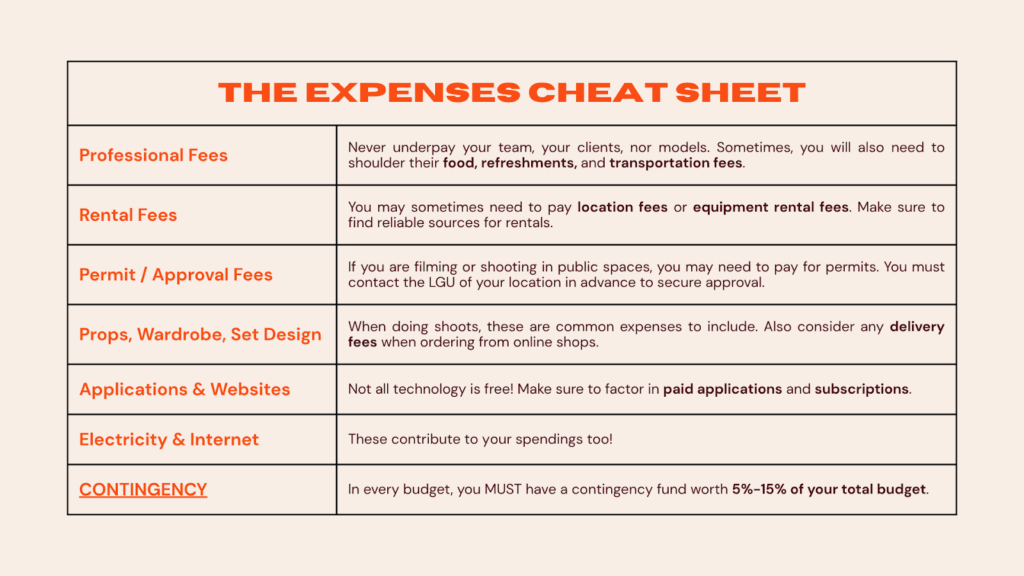

As you navigate the CMP industry, you will encounter different kinds of payments and fees. While it may be daunting to face these concepts, it’s a great first step towards building good financial habits. Luckily for you, Creatives In Progress has prepared a cheat sheet with some fees you might encounter in the industry somewhere along your career. You may want to consider these for your upcoming projects.

Developing your monthly budget

Now that you’re familiar with saving your money and predicting your expenses, you can now develop your budget. When doing this, it’s important to keep your personal and professional budgets separate.

Part 1: Self-Reflection

- Reflect and assess your current financial situation. Ask yourself the following questions:

- Am I earning more than I am spending?

- If my income were to stop right now, would I have enough money to shoulder next month’s expenses?

- What does it mean to me to create a personal budget?

- Set your short-term financial goals, following the SMART framework: specific, measurable, attainable, realistic, and time-bound. Some examples of short-term goals are saving for an emergency fund, investing in a new camera, or paying off certain debts.

Part 2: Making the Budget

There are two main parts when creating a budget: the income and expenses. Your income is the amount of money you receive from different sources, while your expenses are both the fixed and variable things you spend on.

- Choose a budgeting platform that works for you. You can explore different applications or use existing templates on apps such as Google Sheet and Notion.

- Estimate your monthly income from all your sources.

- Estimate your monthly expenses. You can refer to the expenses cheat sheet above.

- If you are encountering new expenses, make sure to do extensive research about how much everything will cost.

- If applicable, you can also refer to past projects to get rough estimates for your expenses.

- Compare your total estimated income and expenses and adjust your budget as needed. If you’re working with a team, make sure that everyone is aligned regarding the total budget.

- Budget all of your expenses following a strategy that works best for you. Below are a few examples of budgeting strategies:

- Zero-Based Budget: Assign every single peso of your income to a specific expense or savings goal. Your total income minus expenses should equal zero.

- Envelope System Budget: Allocate different envelopes for different spendings or savings and add your cash there.

- No-budget Budget: Focus on spending within your means and make sure to set aside cash for savings and extra payments.

- Track your expenses. At the end of the month, reflect on your spending habits and prepare for the next month.

Additional smart budgeting tips

- Always keep your receipts. If you scan them, you can upload them directly to your budget sheet.

- Write down your expenses as soon as you spend them, no matter how small the expense may seem.

- Have an accountability partner who will remind you to stay within your budget.

activities

Activity 1: Reflecting on Financial Habits and Goals

Following the step-by-step process discussed earlier, smart budgeting always begins with self-reflection. For this activity, find a quiet place to reflect and answer the worksheet below.

Activity 2: Creating Sample Budgets

Creating a budget requires critical thinking and problem solving skills. This activity will challenge you to adjust your budget on a case-to-case basis. You may find the activity in this link.

Now that you’re able to budget your money, it’s time to think about your next step: investments! Proceed to the next lesson to learn more about how to help your earnings grow through different means.